VAT and training: watch location rules by client profile

Are you a training provider working with foreign clients? Or do you buy training delivered outside France? The applicable VAT rules are more complex than they appear. A recent tax ruling reminds us of the principles to know.

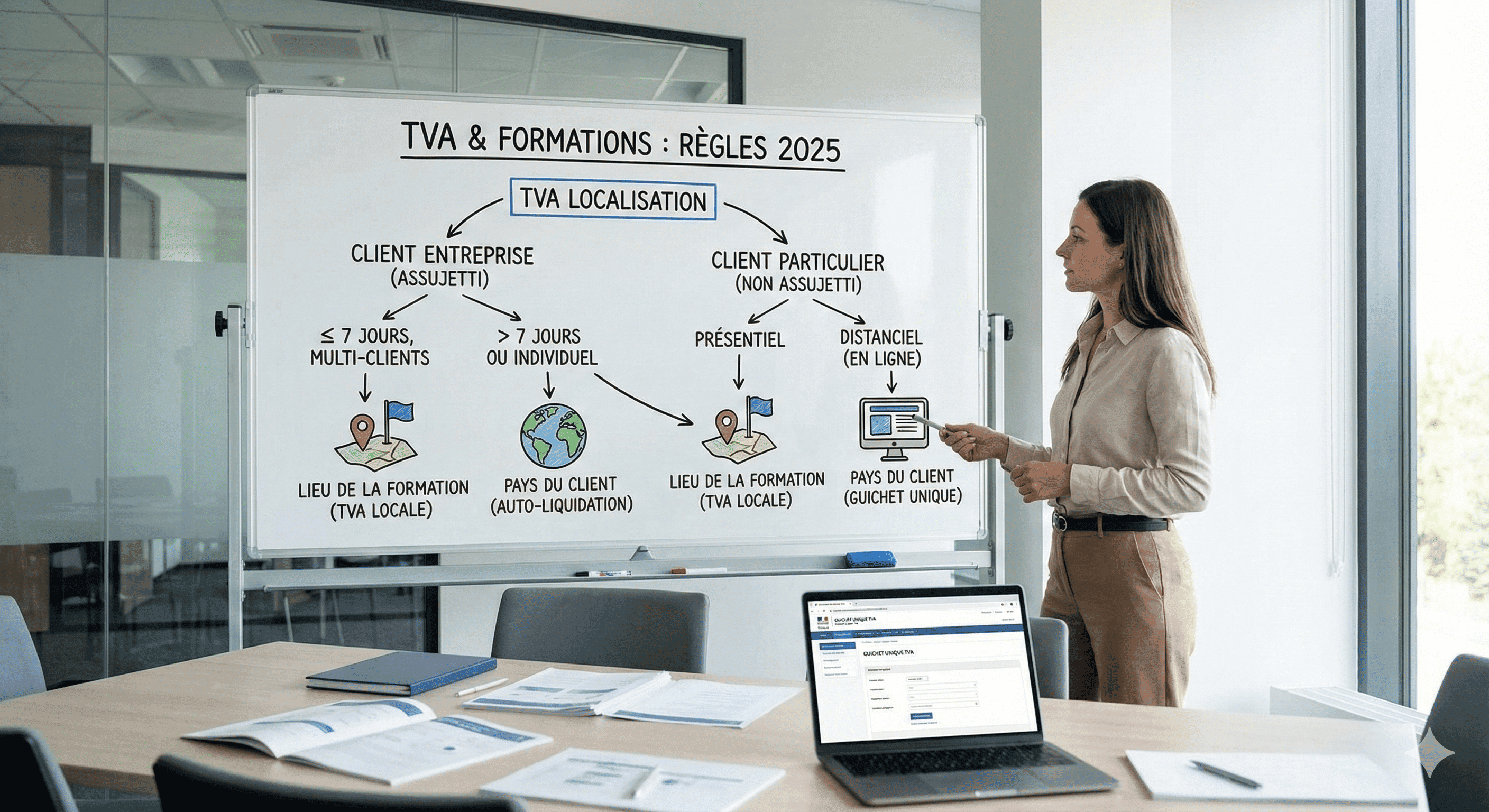

The principle: where is VAT located?

For VAT, the crucial question is always:where is the transaction taxable?The answer determines whether you must charge French VAT, another country's VAT, or no VAT at all.

For training services, the answer depends ontwo criteria:

- Theclient's status: are they VAT-registered or not?

- Theformat of the training: in person, remote, duration...

Case 1: Your client is a business (VAT-registered)

When you sell training to a VAT-registered business, the general rule is simple:VAT is due in the client's country.

In practice:

- Training a French business? French VAT.

- Training a German business? No French VAT; the German business will self-assess German VAT.

The exception: training treated as access to an event

Beware, there is an important exception. Certain training is treated asaccess to an eventand follows a different rule: it is taxablewhere it takes place.

Training is treated as an event if it meets these two conditions:

- It is delivered toseveral VAT-registered persons(not one-to-one training)

- It lasts7 consecutive working days maximum

In that case, if you run a 3-day seminar in Paris for European businesses, you charge French VAT, even if your clients are foreign.

Conversely, 10-day training or training delivered to a single client (even if short) follows the general rule: VAT in the client's country.

Case 2: Your client is an individual (not VAT-registered)

Rules differ for training sold to individuals or organisations not registered for VAT.

In-person training

If the training takes placein person, it is taxablewhere it physically takes place.

Example: you deliver training in Paris to an individual resident in Belgium. You charge French VAT.

Remote training

Since1 January 2025, rules have changed for training deliveredremotely(e-learning, video conference...).

This training is now taxableat the client's establishment.

Example: you sell online training to an individual resident in Spain. Spanish VAT applies. You must either register for VAT in Spain or use the VAT one-stop shop (OSS scheme).

Summary: where to charge VAT?

For business clients (VAT-registered):

When you train several participants in person over 7 days or less, VAT applies where the training takes place. However, if you train a single client in person, whatever the duration, the client's country VAT applies. Likewise, for any training over 7 days, whether in person or remote, VAT is due in the client's country.

For individual clients (not VAT-registered):

In-person training is always subject to VAT where it physically takes place, whatever the duration. For remote training, since January 2025, the VAT of the country where the client resides applies.

Pitfalls to avoid

Misclassifying your client

A client who says they are an "individual" may in fact be a VAT-registered professional. Always ask for theintra-EU VAT numberfor European clients.

Confusing training and event

The 7-day threshold and "several participants" condition are strict. 8-day training is not an event. Neither is 2-day one-to-one training.

Forgetting the 2025 change for remote delivery

If you sold online training to foreign individuals before 2025 with French VAT, check that you now apply the correct rules.

Key takeaways

- Theclient's status(registered or not) is decisive for VAT

- For business clients, VAT is due in their country, except "event" training of less than 7 days

- For individuals in person, VAT at the place of training

- For individuals remotely, VAT at the client's location (since 2025)

- If in doubt, ask your accountant for advice

VAT location errors can be costly: VAT charged incorrectly (not recoverable by the client) or VAT not charged (tax adjustment). Better to secure your practices upfront.